Global Parameter:

|

Description:

|

Earn Interest

|

Earned Interest default setting is TRUE to enable earning interest on available cash.

A False setting disables the interest earning option .

Interest rates used during a simulation are determined by the currency rate files provided in the

Forex Rate file folder for your system base currency:

Forex Rate File Folder Disk Location Preference section of Trading Blox determines which Currency Rate file to use in a test:

Forex Rate Setting Preference Section

In the image example above USD is shown. This setting will use the USD_Rates.txt file records in the Forex Rates folder lending rate to determine the earned interest.

Only the cash amount earns interest:

•Cash for Futures and Forex is the total equity. Money used as margin for futures trading is not deducted from the cash balance since many brokers will allow T-Bills for margin requirements allowing traders to earn interest on the money that is used for margin.

•Cash for Stock class instruments is closed equity minus purchase equity. This means money used to purchase stocks is deducted from the cash balance.

|

Slippage Percent

|

The frictional cost of trading has two components: commissions, and slippage (sometimes also known as "skid"). In actual trading, slippage is the difference between a trade's entry or exit order price, and the price at which the trade is actually filled. In order to accurately reflect the conditions of real trading, the impact of slippage must be simulated during back testing.

|

Minimum Slippage

|

See section in Slippage Percent topic.

|

Max Percent Market Volume

|

Max Percent Market Volume determines the maximum trade size based on a percentage of the current volume. For example, if the volume is 200,000 shares and this parameter is set to 2%, this means that the maximum allowed trade size is 2% of 200,000 or 4,000 shares. If an order is placed for 6,000 shares, it will be reduced to 4,000 shares, and an entry will show in the Filtered Trade Log so that you are aware that the order size was reduced. The volume used is the 5-bar exponential moving average of the volume.

|

Max Margin/Equity to trade

|

The default is 100%, in that if a requested trade would require more than 100% of available equity in margin or cash, then the trade will be filtered. This parameter allows you to mofidy this behavior. If you enter 50 here, the system will filter trades if the new total margin required would be greater than 50% of the total available equity

|

Trade Always on Tick

|

When this parameter is set to false, the system will trade with maximum precision. So if the system buys Gold on a stop at the moving average, which is 365.44789, then the system will buy at that exact value. Conversely it will exit the trade at an exact value as well. The trade price as listed in the trade details will only show the digits of precision of the instrument, as set in the Futures Dictionary, so the trade price would look like 36.45. But the trade profit would not match that value exactly.

When this parameter is set to true, the system will always trade on the tick. It will round up to the nearest tick for buy orders, and down for sell orders. So in the above example, if you placed an order to buy on stop at 365.44789, the system would place the order to buy at 365.45.

The fill prices would also be on tick, so a slippage of 10% could become more as the order price and then fill price gets pushed to a tick.

|

Smart Fill Exit (Smart Exit Fills)

|

When set to true, this function will only fill the exit stop/limit order closest to the open for any particular unit. This can be helpful when using multiple exit blox that place stop/limit orders. If the open is at 10, (and the high is 12 and the low is 7), and you have an exit stop at 11 and a limit order at 8, the stop exit order will be filled.

|

Entry Day Retracement

|

Entry Day Retracement is the percent of the bar range (High-Low) used to compute the trigger price, which determines whether to fill the protective stop on the entry bar.

For a long entry order:

The protective sell stop will be filled if the trigger price is less than or equal to the stop price.

The trigger price is computed as:

' trigger-price cannot be higher than the close or lower than the low.

trigger-price = entry-order-fill-price – (bar-range * entry-day-retracement)

Therefore, using 100% as the entry day retracement is the most conservative approach where the trigger price will be the low of the day, and if the low is less than the protective stop price then the stop will be filled, and the position exited on the entry bar. Note that if on average the fill price is in the middle of the bar, a setting of 50% will on average also use the low of the day as the trigger price.

Using 0% as the entry day retracement is the most aggressive approach where the trigger price will be the close of the day, and if the close is less than the protective stop price, then the stop will be filled, and the position exited on the entry bar.

Using -1 as the entry day retracement will disable this feature, and the protective stop will be ignored for the entry bar.

When orders with a protective price Trading Blox will place the entry-risk points, and order-entry protective price in the order and instrument unit properties, so they are available after the bar of entry.

|

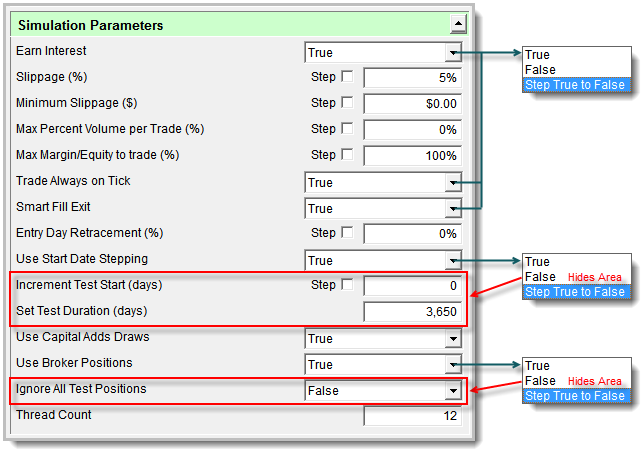

Start Date Stepping

|

Set to true or false to enable or disable the the Increment Test Start option and the Set Test Duration Option

|

Increment Test Start

|

See section in Start Date Stepping topci.

|

Set Test Duration

|

See section in Start Date Stepping topci.

|

Use Broker Positions

|

Set to true to insert the broker positions, as entered in the Broker Position Editor, into the simulation. These positions will be entered for both testing and order generation.

|

Ignore All Test Positions

|

Set to true to ignore all the test generated positions. Use this when the only positions you want in the test, or order generation, are the broker positions. Use Broker Positions must be true for Ignore All Test Positions to have an effect. Often this is used on the very first day of order generation so that you can start with a clean slate and no open positions. If you want a mix of actual positions and theoretical test positions, then leave this box unchecked.

|

Thread Count

|

Global Parameter Thread Count represents the number of test in a stepped simulation that can run at the same time.

Each step in a stepped test runs a complete copy of the Suite’s construction at the same time. This means that a complete copy of the entire Suite’s systems, blox and data files needed to run a test-step is loaded into thread-space memory so it can run as if only one test was being tested.

Trading Blox Builder default license allows two threads. Additional threads can be allowed by accessing your Customer Login section in the Trading Blox Website.

Each computer’s thread count can be between 1 and maximum number allowed by the Trading Blox license. Thread counts should not be more than twice the number of cores in your computer’s CPU. Available memory is important when using a large number of steps in a stepped simulation or when large portfolios are being used. Reducing Optimization Time provides more detailed information about how to judge how many threads would be effective with your computer.

Global parameter Thread Count’s value can easily be changed and saved with each Suite as the needs of each Suite are known.

|

Simulation Scoped Variables

|

Each thread in a multiple thread stepped test contains an entire copy of the Suite’s systems, blox, and data files. This also means that a copy of all the variables and scripts in a suite is contained in each thread.

|