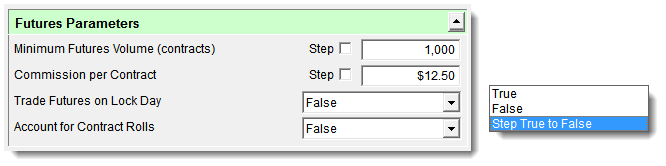

Minimum Futures Volume

|

This parameter applies only to futures. It establishes the minimum daily trading volume, in contracts, required to enter a futures position. It is based on a 5-day exponential moving average of the volume. This value can be viewed by using the instrument.averageVolume property when using the Builder Edition.

|

Commission per Contract

|

This parameter indicates the round-trip charge for each futures contract traded. Assuming a Commission per Contract of $12.50, buying and then subsequently selling 1,000 contracts of sugar would result in a total transaction cost of ($12.50 per contract) x (1,000 contracts) = $12,500.

|

Trade Futures on Lock Day

|

When this parameter is set to false, the simulation will not fill entry or exit orders on days when the high = low, when the trade is in the direction of the lock. The idea is that in futures this could be a lock limit day, and it would be the most conservative assumption to assume you did not get filled.

If you set this parameter to true, you will be filled on these days. This applies to futures only.

Example: With this parameter set to false, and the high equals the low, so it is considered a lock day. If you want to enter long, or exit a short position, and the close of the lock day is less than the close of yesterday, then it will be allowed. But if the close of the lock day is greater than or equal to the close of yesterday, then the fill will be denied.

|

Account for Contract Rolls

|

This parameter applies only to futures, and controls whether or not Trading Blox should account for the increased commission and slippage that would have resulted when rolling contracts when a position is held for a long period of time.

If your data includes the Delivery Month of the futures contract being used on any given day in the backadjusted data, then Trading Blox will use this to determine when to roll. It will account for a roll every time the delivery month changes.

If your data does not include the Delivery Month, Trading Blox will estimate when a roll would occur based on the number of trading months listed in the Futures Dictionary. If you actually roll less often than you have months listed, then you should reduce the list to just the roll months, for most accurate results here.

If there are 4 trading months, then Trading Blox will calculate a contract roll every 3 months. If there are 12 trading months, Trading Blox will calculate a contract roll every month. The first simulated roll will occur in 1/2 the normal roll frequency because, on average, the first contract will be entered with 1/2 its trading life left. This process is based on calendar days and works for intraday, daily, weekly, or monthly data.

Each time a simulated roll occurs, Trading Blox accounts for the roll by deducting slippage and commissions for each contract in the position. The Open Equity is moved to Close Equity. If the futures is non-USD denominated, the currency conversion for the roll date will be used to move profit from open equity to closed. So the profit is locked in at the conversion rate of the roll.

|

Roll Slippage (% of ATR)

|

This option is available when Account for Contract Rolls is set to true.

The slippage used is the roll slippage percent of the Wilder 20-day ATR (39 day non SMA primed Exponential Moving Average of the True Range). This is an un-primed value, and can be accessed by the instrument.default Average True-Range property.

|